Tag: Data & Insights

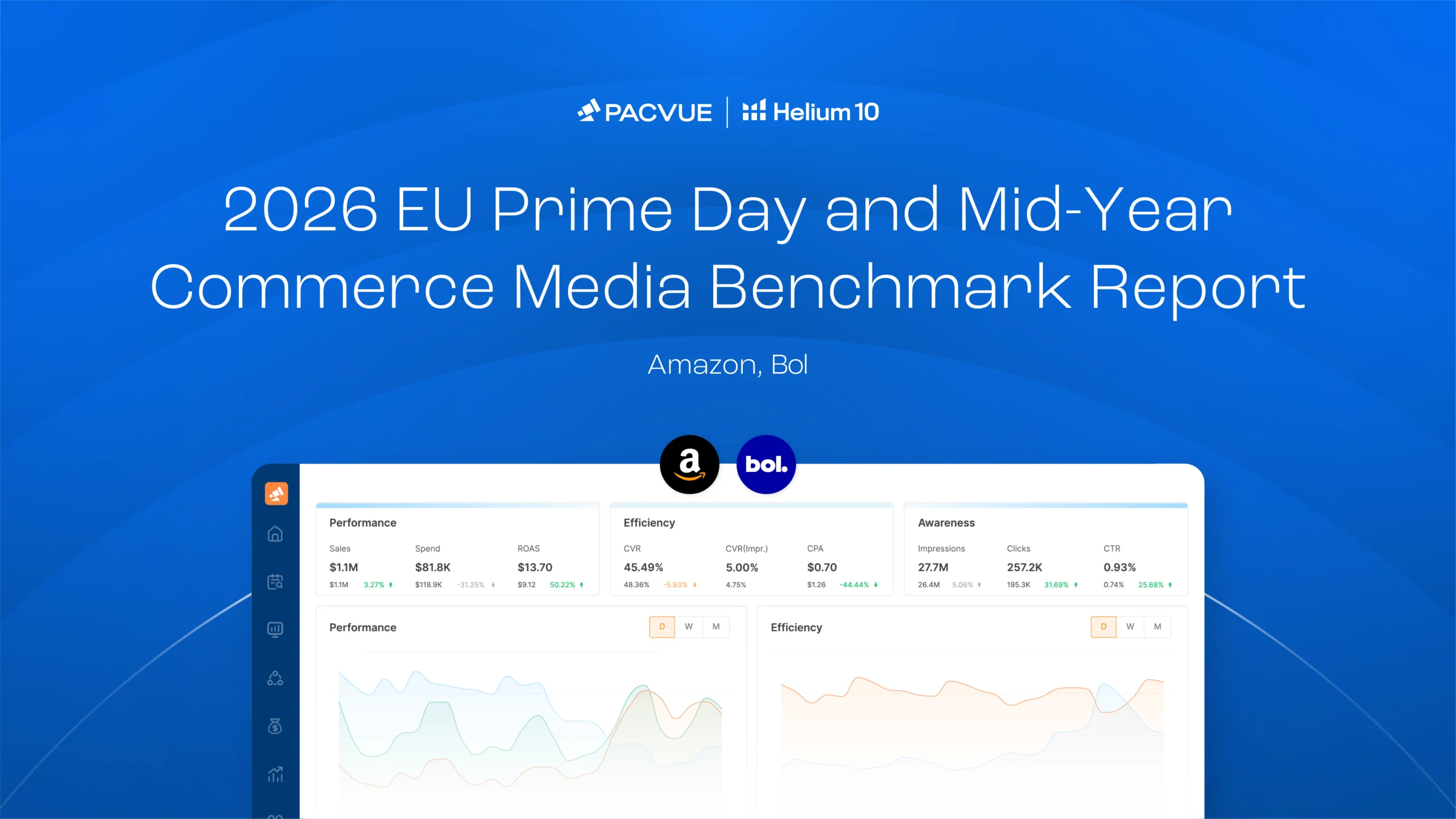

2026 EU Mid-Year Commerce Media & Summer Sales Benchmark Report

Discover how every ad dollar performed across Amazon EU and Bol in Q2 2026 – including promotional events like Prime Day – so you can benchmark and optimize your own campaigns for H2 and beyond.

8 minutes

8 minutes

ChatGPT Ads in 2026: Early Results, Best Practices, and How to Get Started

OpenAI launched ads in ChatGPT earlier this year, and the early campaigns are already teaching us things that don't match what we expected. This guide covers what ChatGPT Ads are, how they work, what the first wave of results is showing, and how to get started, with learnings from a webinar Pacvue hosted with OpenAI and Kepler.

2026 Mid-Year Commerce Media & Summer Sales Benchmark Report

Discover how every ad dollar performed across Amazon, Walmart, Instacart, and Target in Q2 2026—including promotional events like Prime Day—so you can benchmark and optimize your own campaigns for H2 and beyond.

Amazon Business Ads: Building your B2B Retail Media Strategy

Join Pacvue for an in-depth look at how teams are capturing sales from 8MM+ verified business customers. In this session, hear directly from leaders at the front lines of brand demand on what's working, what surprised them, and what it means for your strategy.

7 minutes

7 minutes

What Is Connected TV Advertising? (And Why It Matters for Retail Media)

Connected TV is reshaping how brands reach shoppers before they search. This guide explains what CTV is, how it works, and why it's becoming essential for retail media strategies.

7 minutes

7 minutes

Maintaining Momentum Post Summer Sales Events

Most marketing teams close the tentpole sales window with a sigh of relief. Prime Day, Walmart Deals, Target Circle Deal Days, and Black Friday compound to create some of the biggest new-to-brand opportunities and busiest weeks in the retail media calendar. But when brands treat event days as the finish line, they shut up shop […]

11 minutes

11 minutes

Prime Day in Real Time: Why Hourly Optimization Beats Daily Reporting

Preliminary data from the first days of Prime Day 2026 points to a more competitive summer sales season, with conversion rates under pressure, ad costs climbing, and impressions down. Here's what's driving it and how to optimize your strategy for the final push.

7 minutes

7 minutes

How to Compare Retail Media Performance Across Retailers in Europe

Retail media ad spend in Europe is set to reach €31bn by 20281 The opportunity is growing fast, but so is the cost of getting it wrong. As brands expand across more retail media networks, comparing performance is becoming harder. When clarity slips, budget decisions slow down and revenue opportunities are missed.

7 minutes

7 minutes

AI for Advertising: How Modern Advertisers Can Leverage AI to Drive Growth

If you’re thinking about how to use AI in marketing, the gap between advertisers who use AI and those who don't is widening. AI-powered advertising teams are making better decisions, moving faster, and getting more out of ad budgets. This guide explains what they’re doing differently.

10 minutes

10 minutes

How to Optimize and Scale Amazon DSP Campaigns

Once you understand what Amazon DSP is, the next step is launching, optimizing, and scaling campaigns that move the business. This guide covers how to get started, six ways to optimize performance, how DSP Plus fits into a mature strategy, how non-endemic brands can use DSP, and how Pacvue compares to managing campaigns natively.

14 minutes

14 minutes

What Is Amazon DSP? A Complete Guide for Brands and Agencies in 2026

Amazon DSP (Demand-Side Platform) is Amazon's programmatic advertising platform. It lets brands and agencies buy display, video, audio, and streaming TV ads at scale, reaching audiences on Amazon.com, IMDb, Twitch, Audible, Kindle, and across thousands of third-party sites and apps.

Through the Lens: Making Sense of MCP

Learn how MCP is reshaping commerce media operations. Watch the Pacvue and Parallel Retail Group webinar to hear from leaders scaling without scaling headcount.

Awards & Recognitions